Today's headline on Business Insider: BANK OF AMERICA: "We're heading for an earnings

Today's headline on Business Insider: BANK OF AMERICA: "We're heading for an earnings

recession." This premise has been floated by more than a few analysts and business media personalities. At this point, it is the worst kept secret that a deceleration in earnings growth is being forecast by most stock analysts. The question being asked now is whether the first deceleration in earnings growth in six years will be enough to spark a correction in the stock market with other markets following suit.

It's the Economy Stupid

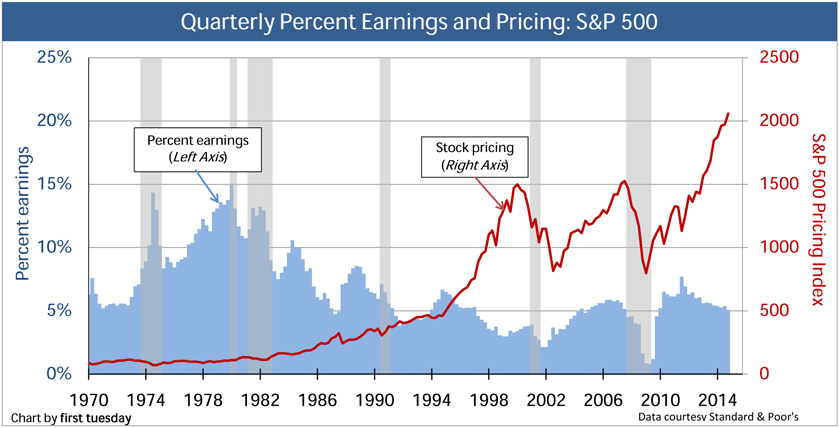

Since the depths of the recession, most observers of the stock market's six-year and counting rise, have viewed it with skepticism and a healthy dose of dubious acceptance. Record earnings growth and an accommodative Fed have contributed to the market's run with market bulls responding to the bear's cynicism by pointing out the strong earnings and low price-earnings multiples as reasons for continued optimism. Now the bulls are faced with a more sober reality: decelerating earnings and their correspondingly higher price-earnings multiples. What will the bulls point to now to justify an ever rising market? With multiples stretched beyond historical norms, asking for yet higher multiples seems unlikely. The chart to the right reflects the S&P 500 valuations (red line) versus declining

earnings (blue wave). There is a discernible departure between price and earnings growth. The only way to justify yet higher prices is a forecast for higher earnings growth going forward. But with forward earnings being reduced, how far out does the market have to look to find brighter skies? How much are investors willing to "pay up" for stocks based on distant earnings? One of the bull's popular refrains over the course of the market's recovery from its lows has been "the second half of the year looks better than the first." A recent concern, admitted by a popular market bull, was of second quarter earnings. The bull confessed that the market could get by with weak first quarter earnings but if second quarter earnings come in weak, it could present a problem for the market. Until now, each market hiccup has been offset by Fed support.

How Long Will the Market Rise on Continued Accommodation?

With earnings growth possibly turning negative, a rising market will look to Fed accommodation to provide bulls with more momentum and will give market bears fuel to feed their growing cynicism. Even market bulls concede that at least a 10% correction would be healthy. But each dip is met with more buying. When is the dip not met by sanguine buyers? Each hint that the Fed will postpone raising its rates is met with a market rally, the most recent happening after the long Easter weekend. A weaker than anticipated labor report was met with a triple digit gain in the Dow Industrials on the first day the market was open after the release of the labor report. How long can this response to the notion of lower rates for longer last? The Fed has already declared that it will be more accommodative for longer and will err on the side of caution and risk being too accommodative. It has tried to be as a transparent as possible and has avoided "surprising" the market with its policies. Although the Fed has expressed a desire to raise rates, it has also conveyed its "patience" to the market about its approach. There will come a point when investors will hit a wall and stop buying at ever higher valuations. That point is probably sooner rather than later. If earnings growth does not reverse and accelerate higher investors will baulk at paying correspondingly higher multiples as their risk profile is breached. What is the market's fair value in a permanent zero-rate environment? If investors never anticipated higher rates, what bid would they place on stocks? In a zero-rate world, a new metric would need to be used as a risk comparison. US treasuries would not be appropriate or adequate. Maybe a foreign bond rate or inflation (CPI) becomes the new risk barometer.

It's the Market Stupid

The Fed may choose not to raise rates based upon the performance of the economic data points they follow before the markets ultimately force their hand. The market has already disagreed with the rate forecast the Fed had been describing only to have their views confirmed by the Fed's actions to postpone raising. The same may prove to be true regarding when the Fed needs to raise rates. The market will be ahead of the Fed when they should raise rates. The market will not accept lower rates and will demand higher returns. This will cause rates to rise and stocks to pull back accordingly. When does this happen? As soon as the risk-return profile for investors shifts and capital flees US markets for greener pastures. Those greener pastures will have German, French, Spanish and Italian accents. As the Euro zone heals and growth improves, US capital will find its way over the Atlantic in a meaningful way. This process has already started. The ECB is in the nascent stage of its own QE program and has a ways to go, allowing for further easing and additional stimulus. If capital finds its way overseas in a meaningful way, the next dip in the US may not finds its fair share of buyers.

How Long Will the Market Rise on Continued Accommodation?

With earnings growth possibly turning negative, a rising market will look to Fed accommodation to provide bulls with more momentum and will give market bears fuel to feed their growing cynicism. Even market bulls concede that at least a 10% correction would be healthy. But each dip is met with more buying. When is the dip not met by sanguine buyers? Each hint that the Fed will postpone raising its rates is met with a market rally, the most recent happening after the long Easter weekend. A weaker than anticipated labor report was met with a triple digit gain in the Dow Industrials on the first day the market was open after the release of the labor report. How long can this response to the notion of lower rates for longer last? The Fed has already declared that it will be more accommodative for longer and will err on the side of caution and risk being too accommodative. It has tried to be as a transparent as possible and has avoided "surprising" the market with its policies. Although the Fed has expressed a desire to raise rates, it has also conveyed its "patience" to the market about its approach. There will come a point when investors will hit a wall and stop buying at ever higher valuations. That point is probably sooner rather than later. If earnings growth does not reverse and accelerate higher investors will baulk at paying correspondingly higher multiples as their risk profile is breached. What is the market's fair value in a permanent zero-rate environment? If investors never anticipated higher rates, what bid would they place on stocks? In a zero-rate world, a new metric would need to be used as a risk comparison. US treasuries would not be appropriate or adequate. Maybe a foreign bond rate or inflation (CPI) becomes the new risk barometer.

It's the Market Stupid

The Fed may choose not to raise rates based upon the performance of the economic data points they follow before the markets ultimately force their hand. The market has already disagreed with the rate forecast the Fed had been describing only to have their views confirmed by the Fed's actions to postpone raising. The same may prove to be true regarding when the Fed needs to raise rates. The market will be ahead of the Fed when they should raise rates. The market will not accept lower rates and will demand higher returns. This will cause rates to rise and stocks to pull back accordingly. When does this happen? As soon as the risk-return profile for investors shifts and capital flees US markets for greener pastures. Those greener pastures will have German, French, Spanish and Italian accents. As the Euro zone heals and growth improves, US capital will find its way over the Atlantic in a meaningful way. This process has already started. The ECB is in the nascent stage of its own QE program and has a ways to go, allowing for further easing and additional stimulus. If capital finds its way overseas in a meaningful way, the next dip in the US may not finds its fair share of buyers.