In the aftermath of the terrorist attacks in Paris on Friday the 13th, equity markets around the globe staged impressive gains on Monday, the first trading day after the attacks. Before the tragic events in Paris, analysts and market pundits had speculated whether markets had it in them to stage a traditional "Santa's" rally this season or if markets had seen most of their gains for the year after the slump in August and September. The question is: Does the market have any more juice?

The Obstacles

History and data seem to reflect market strength during the traditional holiday season, beginning in November. The attacks in Paris represent one obstacle to positive gains this holiday, but what other hurdles must the market overcome to give investors reason to cheer?

Commodities

There seems to be a strong correlation between the price of oil and equity prices. How long will this relationship last? For the time being, weak oil means weak equities. Has oil found a bottom near $40 or will we see further weakness? Because of the correlation with equities market cheerleaders are calling a bottom in oil. So far, they have been wrong on this.

There was a time when copper was fondly referred to as "Doctor" Copper. This was because copper was considered a metric for industrial and manufacturing production because so many items used copper in the manufacturing process. So went copper prices so went markets. This relationship seems to have ended either because it never really carried any real weight or because it stopped suiting the pundits that needed a "story" for the market to rise. Regardless, copper is down 30% this year alone and reflects weak demand from major industrial countries as well as China.

Strong Returns Booked in October

The sell offs in August and September set up October for massive gains, the best month in 4 years. The S&P 500 logged a gain of 8.3% and the Dow Industrials logged a gain of 8.5%. After this impressive comeback many analyst questioned what was left in the tank for the holidays and year end. Some of the Street's biggest bulls are sticking to their early forecasts for further gains but most have trimmed their expectations. The argument is that October pulled traditional late year gains forward.

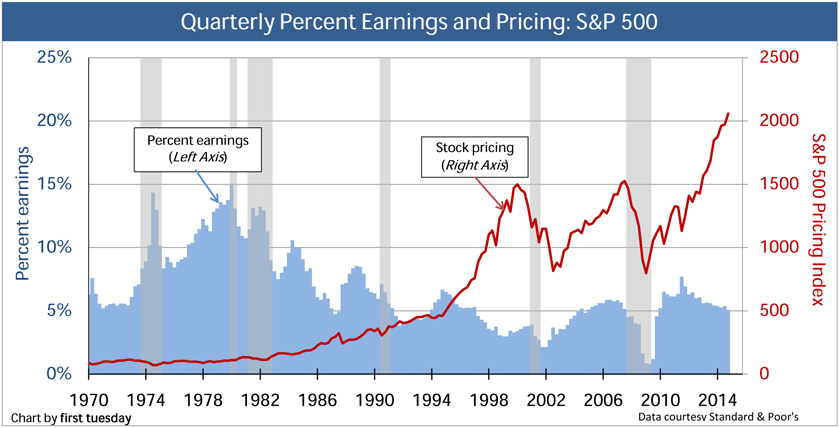

Weak Fundamentals with Healthy Valuations

Corporate earnings have been coming down raising the overall market's P/E ratio with them. With October's stellar returns the price of the overall market is not cheap and as earnings fall the market gets more and more price. Further gains are challenged by these multiples and no one, even the staunchest bulls, are calling for multiples to expand at this point as the growth required to accompany them is not visible at this point in the cycle.

The Fed's December Meeting

Futures forecast a 70% chance of a Fed rate HIKE in December. This is elevated after a strong October labor report and decent wage gains. The market wants a rate increase but will it rue what it wishes for when it finally comes? Equity gains in the face of rising interest rates is not out of the question, and maybe will come with a sigh of relief, but it's not traditional that equities rally on tightening credit.

Flat 2015

The S&P 500 was flat for the year as of this publishing. Given the headwinds and strong bounce in October, markets will likely end the year near where they currently stand. After the Fed FINALLY raises rates at its December meeting, analysts will try to forecast markets in 2016 and the future path of rates and its effect on equities. There will always be bulls and there will always be bears and the markets will do what they will.

The Obstacles

History and data seem to reflect market strength during the traditional holiday season, beginning in November. The attacks in Paris represent one obstacle to positive gains this holiday, but what other hurdles must the market overcome to give investors reason to cheer?

Commodities

There seems to be a strong correlation between the price of oil and equity prices. How long will this relationship last? For the time being, weak oil means weak equities. Has oil found a bottom near $40 or will we see further weakness? Because of the correlation with equities market cheerleaders are calling a bottom in oil. So far, they have been wrong on this.

There was a time when copper was fondly referred to as "Doctor" Copper. This was because copper was considered a metric for industrial and manufacturing production because so many items used copper in the manufacturing process. So went copper prices so went markets. This relationship seems to have ended either because it never really carried any real weight or because it stopped suiting the pundits that needed a "story" for the market to rise. Regardless, copper is down 30% this year alone and reflects weak demand from major industrial countries as well as China.

Strong Returns Booked in October

The sell offs in August and September set up October for massive gains, the best month in 4 years. The S&P 500 logged a gain of 8.3% and the Dow Industrials logged a gain of 8.5%. After this impressive comeback many analyst questioned what was left in the tank for the holidays and year end. Some of the Street's biggest bulls are sticking to their early forecasts for further gains but most have trimmed their expectations. The argument is that October pulled traditional late year gains forward.

Weak Fundamentals with Healthy Valuations

Corporate earnings have been coming down raising the overall market's P/E ratio with them. With October's stellar returns the price of the overall market is not cheap and as earnings fall the market gets more and more price. Further gains are challenged by these multiples and no one, even the staunchest bulls, are calling for multiples to expand at this point as the growth required to accompany them is not visible at this point in the cycle.

The Fed's December Meeting

Futures forecast a 70% chance of a Fed rate HIKE in December. This is elevated after a strong October labor report and decent wage gains. The market wants a rate increase but will it rue what it wishes for when it finally comes? Equity gains in the face of rising interest rates is not out of the question, and maybe will come with a sigh of relief, but it's not traditional that equities rally on tightening credit.

Flat 2015

The S&P 500 was flat for the year as of this publishing. Given the headwinds and strong bounce in October, markets will likely end the year near where they currently stand. After the Fed FINALLY raises rates at its December meeting, analysts will try to forecast markets in 2016 and the future path of rates and its effect on equities. There will always be bulls and there will always be bears and the markets will do what they will.